This article is more than 1 year old

Don't Hammer Bob's backup biz: At least sales are up

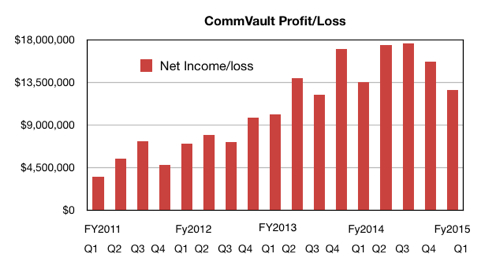

Profits are down at CommVault but it's still beating Wall St

CommVault, the all-singing-and-dancing data management, enterprise backup and archive company, saw its revenues rise 14 per cent in its first fiscal 2015 quarter - but its profits fell by five per cent. Despite that, it still beat Wall Street's earnings estimates.

Revenues were $152.6m compared to $134.4m a year ago, while the firm posted a profit of $12.7m; it was $13.5m at the same point last year, meaning net income dived by five per cent.

As a percentage of revenues, net income was 8.32 per cent, continuing a decline since the third fiscal 2014 quarter when the percentage was 12.26 per cent. Since then, the percentage figure has been 11.48 and 10.01 per cent.

- The quarter saw software revenues of $72.1m, 10 per cent up year-over-year but nine per cent less than the previous quarter. Wall Street was expecting 8 per cent y-o-y.

- Services revenue was $80.6m, up 17 per cent annually and four per cent sequentially.

Last quarter CommVault stumbled a bit, under-performing according to Wall Street. This quarter it was back on track.

Analyst haus Stifel Nicolaus' MD, Aaron Rakers, noted in a written update: “CommVault’s sub-$100k deal implied revenue declined 10 per cent yr/yr and -22 per cent sequentially. (First yr/yr decline since June 2010.) The shortfall in sales staff noted last quarter has been fixed with 100 new employees this quarter, mostly in field sales. More sales heads are coming.”

Bob Hammer, CommVault’s chairman, president and CEO, said of the results: “We began fiscal year 2015 with a solid first quarter, which was highlighted by year-over-year revenue growth of 14 per cent and year-over-year operating cash flow growth of 44 per cent. Our year-over-year revenue growth was driven by a record percentage of enterprise software revenue (software transactions greater than $100,000), a record average enterprise deal size and solid results from our services organisation.”

William Blair analyst Jason Ader said: “The company's ramped-up investment plan… will not yield top-line results until the second half of the fiscal year at the earliest.”

So what has CommVault got coming? Look no further than Simpana 10 R2, expected in the next few weeks, which Ader says, “should drive incremental sales and improve SMB sector positioning.”

But there are reasons to be cautious, according to Blair. “The September quarter is expected to be challenging given a depleted large deal pipeline exiting the June quarter and a weaker-than-normal federal performance, requiring a steep revenue ramp-up in the second half of the year.… management noted that CommVault has become increasingly dependent on large deals whose timing is inherently unpredictable.”

The subsequent second half of fiscal 2015 should be better, though.

Ader and Rakers both discussed Simpana 10 R2, noting it should improve CommVault's competitive standing against newer SMB players, such as Actifio, Veeam, and Code42. It will feature:

- Simplified packaging and new pricing that will make it easier for customers to acquire Simpana-based systems that solve specific issues

- Cloud lifecycle management

- Stand-alone options for virtual machine management (anti-Veeam)

- Variant offering native/live copy management (anti-Actifio)

- Stand-alone mobile variant with enhanced functionality

- Office 365 e-mail archiving managed both on- and off premise

- New security information and event management

- Introduction of an appliance program

- Workflow orchestration and automation

- Pattern matching (similar to Splunk)

- Database archiving including Oracle DBs

Rakers said: “CommVault … may also introduce additional Simpana 10 R2 standalone solutions focused on disaster recovery, test/dev, and cloud archiving.”

In Ader’s view, “the backup market remains in transition with an accelerated shift to cloud-based delivery models, especially in the SMB segment; a transition to subscription-based cloud pricing models; and extended refresh cycles for many customers.”

Ader also notes CommVault was early in its move to support the cloud and has more than 200 cloud service provider customers. But he worries that “the shift to cloud-based backup could have a deflationary effect on the overall backup market given the pricing power of large cloud operators.”

However, “CommVault remains a high-probability takeout candidate, in our view, with a healthy number of potential suitors.”

Who might they be?

Its market capitalisation is $2.3bn, so wannabe buyers would need a $2.5bn - $3bn war chest. EMC, IBM and Symantec would need to see Simpana offering great incremental revenue opportunities that compensated for reduced sales of their existing legacy products like Legato, Backup Exec and Tivoli protection software for CommVault to be an attractive buyout proposition. Dell and HP also have existing backup products. NetApp doesn't, though. HDS might also be a potential suitor. ®