This article is more than 1 year old

If you work on Seagate's performance drives, time to find another job

Lousy three months ends multi-year stream of profit

+Comment As expected, Seagate's revenues totaled $2.6bn in the three months to April 1, the third quarter [PDF] in its fiscal 2016, down 21 per cent year-on-year.

And as anticipated, it made a $21m loss – its first loss in many many quarters and way down from the year-ago's $291m profit.

On Friday, as the results for Q3 were published, chairman and CEO Steve Luczo was blunt: “Our quarterly results fell short of our expectations as a result of several near-term demand factors. Despite these challenges, we believe we have the product portfolio, technology roadmap and operational leverage to ensure we are well-positioned for long-term success. Accordingly, we are aggressively working to position Seagate to respond to new demand levels and are committed to ongoing financial discipline.”

He is still pinning his hopes to capacity storage growth: “Although the short-term dynamics of our industry are challenging, we continue to see significant and growing exabyte demand, particularly as enterprise applications shift to cloud environments.

"As we look forward, our strategic focus is unchanged – we are broadening our storage portfolio to meet the needs of our growing global customer base, building upon our strong competitive position and optimizing our business for continued financial performance. These focus areas will enable us to build lasting value for shareholders.”

Hard drive revenue was $2.37bn (down 22 per cent from last year's $3.1bn), while enterprise systems, flash and other tech brought in $224m (down 2.2 per cent year-on-year) in spite of a Dot Hill contribution.

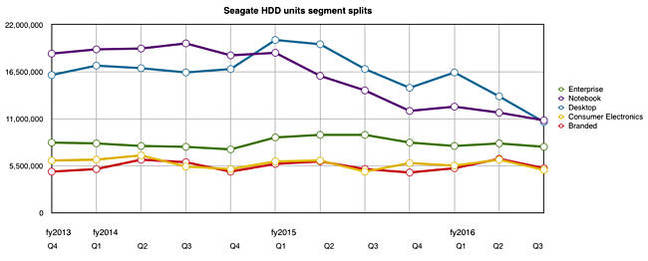

It shipped 39.2 million disk drives in the quarter, down from 45.9 million in the previous quarter and 50.1 million a year ago. The main damage to these figures was done by a continuation of the desktop drive decline, which fell below the notebook drive numbers.

Average capacity per drive grew to 1,417GB. So far growth in the number of exabytes shipped per quarter is not really evident, the numbers being 54.6, 51.7, 55.2, 60.6 and 55.6EB over the past five quarters to date. Enterprise performance drives are going to flash; Seagate noted that it saw a 700,000 shortfall in those units versus its expectations in the quarter. Notebook drives are going to flash. Desktop drives are going to flash. Enterprise capacity drives are not taking up the slack, with Seagate only just catching up with WD’s helium-based 10TB drives this quarter as far as volume shipping is concerned.

Seagate is so far behind in SSD sales it doesn’t even call out the flash drive numbers separately in its public charts.

Stifel MD Aaron Rakers said Seagate exhibited “the lowest gross margin percentage we have seen since September 2011.” He pointed out that Seagate’s ”high-cap (nearline) HDD units totaled 4.5 million, up from 4.4 million units in the prior quarter and down from 4.7 million units shipped in the year ago quarter.”

“Mission-critical enterprise HDD shipments totaled 3.2 million units, down from 3.7 million and 4.3 million units shipped in the prior and year ago quarters,” we're told.

Seagate is facing long-term disk drive demand changes. Previously Luczo had said: “The company is in the process of prioritizing our strategic positioning, manufacturing footprint and operating expense investments to achieve the appropriate level of normalized earnings. We anticipate that these actions will be implemented over the next several quarters.”

We anticipate drive manufacturing capacity reductions are coming, with potential workforce cuts and some market sector defocussing.

Rakers said Seagate has a plan to reduce its HDD manufacturing capacity footprint by 35 per cent, saving approximately $20m per quarter. Fourth quarter revenue is expected to be $2.3bn, down from last year's $2.9bn, and full fiscal 2016 revenues are anticipated to be $10.8bn, down 21.2 per cent on last year's $13.7bn. Not good.

Register comment

It is El Reg’s opinion that enterprise drive SSD substitution will potentially cause devastating reductions in performance drive shipments. No one knows the actual numbers involved, but if a 2U 12-SSD array can stand in, performance-wise, for 60 performance disk drives, representing a 5:1 drive count reduction, then 10,000 enterprise SSD shipments equates to 50,000 fewer enterprise HDD shipments.

If the drive count reduction ratio is 10:1 then 100,000 enterprise SSD units sold means 1,000,000 fewer enterprise performance HDD sold. Four quarters of that and four million performance disk drives are no longer needed. Imagine you are now in charge of Seagate (and WD) performance drive production planning: time to get another job.

Another “if”: if 3D TLC NAND SSDs start replacing nearline disk drives then the disk drive production planning misery mounts up even further. At least WD can offset lost HDD revenue to some extent against SSD revenue. Seagate does not even have that compensation. This lack of a flash focus will come to be seen, we think, as a terrible misstep by Steve Luczo. ®